Streamline Your Payments: Discover the Convenience of myccpay com Payment

Discover the convenience of myccpay.com payment! Streamline your payments with ease and manage your finances effortlessly.

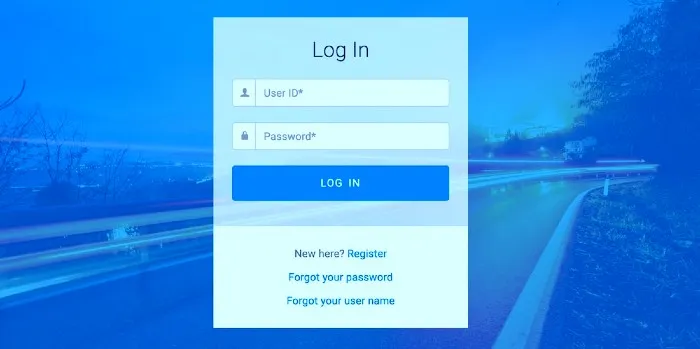

MyCCPay – Official Login Portal at www.myccpay.com

Discover the convenience of myccpay.com payment! Streamline your payments with ease and manage your finances effortlessly.

Discover the advantages of the myccpay application – seamless financial management at your fingertips! Simplify payments, enhance security, and gain convenient account access. Try myccpay today!

Master the myccpay.com Revvi Sign In App for effortless payments! Create an account, make payments, and stay in control.

Empower your financial journey with www.myccpay.com register. Unlock the benefits and features of myccpay for seamless money management.

Empower your financial freedom with MyCCPay! Connect easily via phone for seamless assistance. Find MyCCPay phone number now!

Discover the power of myccpay Total for financial management – track balances, schedule payments, and gain control!

Discover the benefits of myccpay login! Streamline your payments with convenient account management and secure transactions. Log in now!

Mastering MyCCPay login! Get the ultimate guide to unlock your account and troubleshoot login issues like a pro.

Discover the robust page security protocols of myccpay.com. Keep your personal information safe and sound with SSL encryption and more!

Unlock the magic of myccpay credit cards! Seamlessly manage transactions, payments, and account balance with ease.